Amazon Deep Dive: AWS Re-Accelerates, $200B AI Capex, and the Anthropic Flywheel—AMZN Is Being Repriced

AWS just posted its fastest growth in 15 quarters at +28% YoY, but the real story is Amazon's $200B capex bet on AI infrastructure—funded by retail, ads, and subscriptions. The Anthropic partnership deepens the flywheel, but free cash flow tells a harder truth.

TL;DR · The One-Line Thesis

Amazon's 2026 story is no longer "e-commerce + cloud." It's using retail, advertising, and subscription cash flows to fund a high-stakes capex bet on next-generation AI infrastructure.

- AWS re-accelerating: Q1 revenue $37.6B, +28% YoY — the fastest growth in 15 quarters[Yahoo]; management disclosed AI-related services run-rate has exceeded $15B

- Advertising and custom silicon both accelerating: Ads at $17.2B, ~+22%–+24% YoY (methodology varies)[Investing.com]; Jassy disclosed on the earnings call that the custom silicon business (Graviton + Trainium + Nitro) exceeds $20B run-rate (not a separately reported segment)

- The price tag: capex: Q1 capex of $44.2B (cash capex ~$43.2B, methodology varies), +76% YoY; full-year guidance holds at ~$200B[AlgeriaTech]; TTM free cash flow compressed to $1.2B[TNW]

- Anthropic flywheel deepening: Amazon committed up to $25B in additional investment on 4/20[CNBC] → Anthropic pledged $100B+ in AWS purchases over the next decade and access to up to 5 GW of compute[The New Stack]; whether this translates to high ROIC hinges on Trainium validation at scale, AWS margin recovery, and data center utilization

- Alexa+ reaching scale: Rolled out free to U.S. Prime members on 2/4 (third-party CIRP estimates a base of 200M+)[GeekWire]; on 5/13 Amazon launched Alexa for Shopping, unifying the Rufus and Alexa+ shopping experience[Axios]

- Market pricing: Analyst consensus average target $306 / median $315 (+13% upside)[Stock Analysis] — mildly constructive but not a high-conviction crowded trade

- Near-term swing factors: Q2 tariff pass-through, the FCF narrative under capex pressure, and whether Trainium penetration can drive AWS gross margin improvement

Run-rate: An annualized revenue figure extrapolated from the current quarterly pace. Common on earnings calls; not an audited segment disclosure.

⭐ OurAlpha's Core View

The market is repricing Amazon away from "earnings growth" and toward "AI capacity ROIC." AWS re-acceleration is just the first layer. What will actually drive a valuation re-rating over the next 12–24 months is whether $200B in capex converts into higher AWS growth, lower unit compute costs, and a credible free cash flow recovery path.

OurAlpha's stance on AMZN: medium-term constructive, but not a near-term momentum play.

- Near-term headwinds: $200B capex overhang and declining free cash flow

- Medium-term re-rating catalysts: AWS margins, Trainium penetration, advertising profit contribution

- Long-term optionality: Whether Alexa for Shopping becomes the default AI commerce entry point

Best suited for investors with a 2–3 year horizon, not tactical capital looking for a significant move over 3–6 months.

OurAlpha Score

| Dimension | Score | Notes |

|---|---|---|

| News Intensity | 4 / 5 | Earnings + Anthropic + Alexa+ + Trainium catalysts converging |

| Market Sentiment | Neutral-to-Bullish | Analysts at Strong Buy; post-earnings AH saw initial pop then fade as capex concerns spread |

| Trend Status | Strong (near-term chop) | Long-term AI narrative intact; capex overhang should be absorbed within 12 months |

| Retail Risk | Medium | Upside and downside both in play — no obvious edge |

Q1 2026 Earnings: Beat on the Surface, Cracks Underneath

After the close on April 29, Amazon delivered a clean, across-the-board beat[Yahoo][TNW]:

| Metric | Actual | Consensus | vs. Estimate |

|---|---|---|---|

| Revenue | $181.5B | $177.3B | +2.4% |

| EPS | $2.78 | $1.64 | +70% (incl. $16.8B Anthropic mark-to-market gain) |

| AWS Revenue | $37.6B (YoY +28%) | YoY +26% | Fastest growth in 15 quarters |

| Advertising Revenue | $17.2B (YoY +22%–+24%, methodology varies) | YoY +21% | Continued acceleration |

The post-earnings stock reaction was two-sided: AWS's upside provided initial support, lifting shares nearly 4% in after-hours trading, but $200B in capex and broadening free cash flow pressure capped multiple expansion, and shares subsequently gave back roughly 3% in a later after-hours leg.

Capex: Q1 Up 76% YoY

Capex figures vary slightly across sources: the company's own financial definition puts cash capex at ~$43.2B, while some outlets cite a broader capex figure of ~$44.2B[Investing.com]. The two are not directly comparable, but the core takeaway is unchanged: Q1 capex surged roughly +76% YoY (vs. ~$25B in the prior-year period), driven primarily by AI data centers and chip capacity buildout.

Q1 results further confirmed the full-year 2026 capex framework of ~$200B (the market had already begun pricing this in after Q4 2025 earnings — it was not a new disclosure in Q1), representing a 56% step-up from 2025's $128B[AlgeriaTech]. This is an extraordinary capex intensity by Amazon's historical standards, making it one of the most aggressive participants in the current Big Tech AI capex cycle.

Free Cash Flow: TTM Falls to $1.2B

The headline EPS was flattered by a $16.8B non-cash mark-to-market gain on Amazon's Anthropic stake[TNW]. Strip that out, and trailing twelve-month free cash flow (TTM through 3/31/2026) was just $1.2B, weighed down primarily by AI and data center capex — prompting the market to shift its lens on Amazon from earnings growth to return on invested capital.

The market's verdict was clear: the acceleration story across cloud, advertising, and chips gets credit, but the FCF drag from $200B in capex demands a repricing. That is the fundamental reason Amazon has broken out of the simple beat-and-re-rate playbook that worked in 2024 — it is evolving into a compute infrastructure company, and the valuation framework needs to migrate from P/E to capacity ROIC.

II. AWS Re-accelerates to 28%: The Story Holds, But at What Cost

AWS was the most unambiguous bright spot in this earnings report. Q1 revenue came in at $37.6B, up 28% YoY — the fastest growth rate in the past 15 quarters (nearly four years). To put that in context, AWS growth had dipped into the 12% range in early 2024, a period when the market was seriously questioning whether AWS could still outrun Microsoft Azure and Google GCP.

This isn't simply a cloud demand recovery — it's AI workloads moving into production, driving concurrent demand across inference, training, data services, and enterprise deployment infrastructure.

The re-acceleration is being driven by three forces.

1. Enterprise AI Workloads Move from Pilot to Production

Bedrock (Amazon's managed multi-model LLM platform) saw inference call volume grow multiples year-over-year in Q1. Per management commentary and press reports, AWS AI-related services have surpassed a $15B run-rate (versus under $5B in the same period last year)[AlgeriaTech]; note that Amazon does not report "AI revenue" as a standalone segment.

2. Anthropic: One Customer, One Massive Contract

Anthropic has committed to $100B+ in AWS spend over the next decade with access to up to 5 GW of capacity[The New Stack], the majority of which is training compute and Trainium chip consumption. This backlog is a key variable underpinning AWS's ability to sustain its growth trajectory.

3. Existing Customers Double Down

Management disclosed on the earnings call that renewal values on existing customer contracts rose materially year-over-year — only the second time this pattern has emerged since the pandemic-era cloud migration wave. The underlying driver: enterprises deploying their own GPT/Claude/Llama applications into production and needing reliable, committed cloud capacity to do it.

But sustaining this acceleration requires capacity that must be built ahead of demand. The compute needed to support 28% growth must be underpinned by data centers and GPU/Trainium infrastructure laid down 12–18 months in advance — which is precisely why capex has to scale from $128B to $200B.

This is also a good moment to introduce a concept central to understanding how US equities are priced — Price In (whether the market has already discounted a development).

Has the market priced in AWS's 28% growth? The answer: the narrative is priced in; the cadence is not.

The market has long expected AWS to accelerate on the back of AI — the open questions were how high and for how long. When Q1 actually printed 28%, the stock reaction was muted, because the result landed within the expected range — that's what it means for a narrative to be priced in. The real marginal information is whether AWS can sustain 28% or better through Q2–Q4. That's where the new debate lives. The current consensus pencils in 25%–30% growth for the remainder of the year. Any print outside that band is what actually moves the stock.

III. Anthropic + Trainium: The Underappreciated Vertical Loop

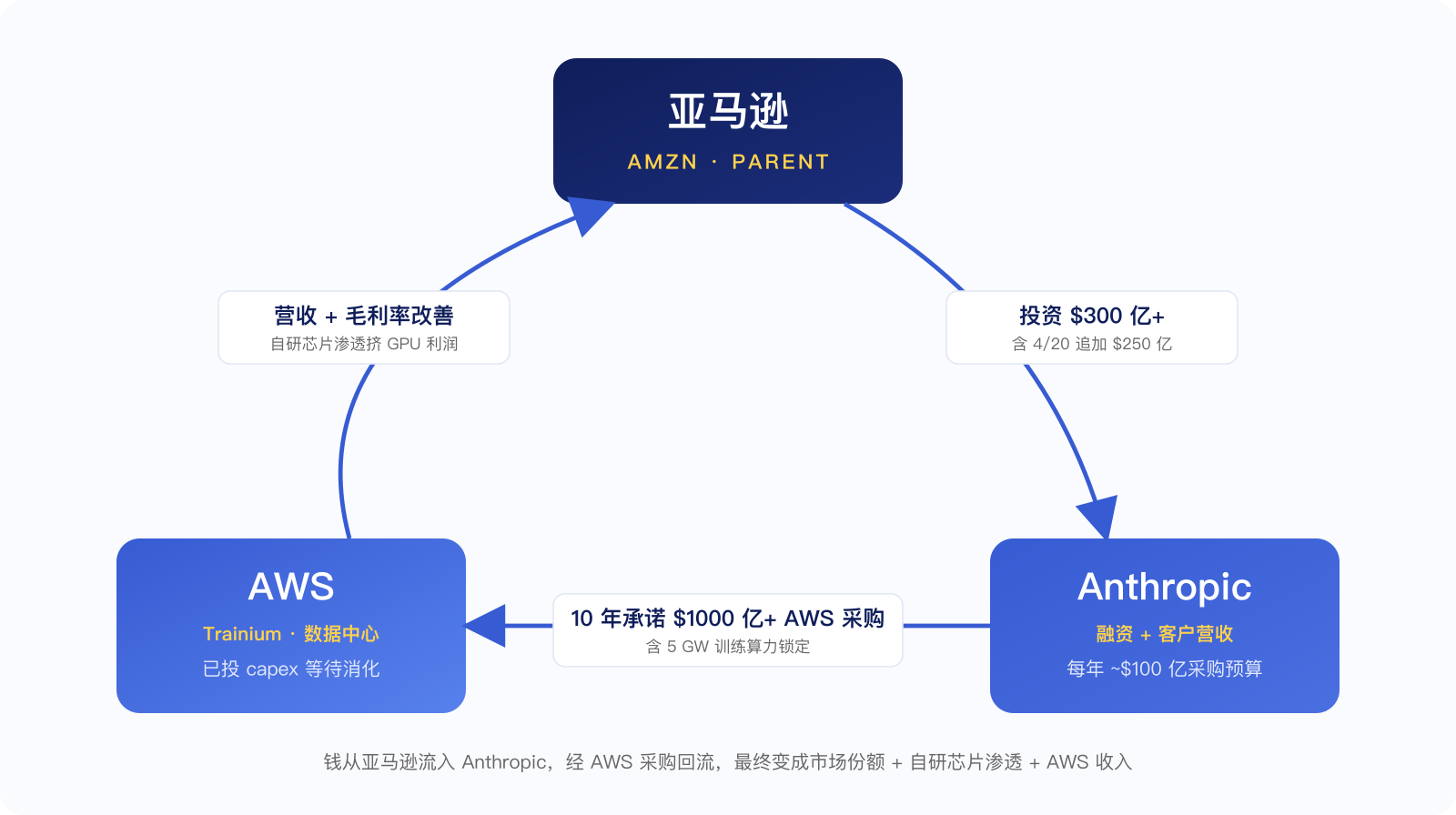

On April 20, Amazon announced it will immediately deploy an additional $5B into Anthropic, with milestone-based top-ups of up to $20B more[CNBC]; combined with the ~$8B already deployed, cumulative capital in stands at ~$13B today, and if all milestones trigger, Amazon's total committed investment in Anthropic would exceed $30B. Separately, Anthropic committed to spend >$100B on AWS over the next decade and secured up to 5 GW of compute capacity[The New Stack]. The numbers are staggering on their face. But if you walk away thinking "Amazon is just backing an AI company," you've missed the point entirely.

This is a triangular closed loop:

This is not a simple "invest in an AI company" play. It is Amazon using an equity stake to lock in a hyperscale model customer, then closing the demand loop through long-term AWS contracts, proprietary Trainium chips, and data center buildout.

But this loop is not risk-free arbitrage. Anthropic's procurement commitments will be fulfilled gradually over the next decade, and Amazon's deployed capital will not convert into AWS revenue immediately or linearly. The real questions are whether Anthropic's model demand can sustain its growth trajectory and whether Trainium can prove its cost-performance advantage at scale across training and inference workloads. In other words, the "closed loop" is a thesis, not a conclusion.

The playbook isn't without precedent—Microsoft ran the same structure with OpenAI. But what differentiates Amazon is the proprietary silicon angle.

Trainium business: real progress (per management)[AlgeriaTech]:

- Trainium2 ramped to mass production in mid-2025; Jassy disclosed on the Q1 earnings call that it delivers ~30% better price-performance versus comparable GPUs, and by early 2026 was "largely sold out"

- Trainium3 began shipping in Q1 2026; Jassy characterized it as "nearly fully subscribed"

- Jassy also disclosed that the proprietary silicon business (Graviton + Trainium + Nitro) combined run-rate has exceeded $20B, growing at triple-digit year-over-year rates

- Important caveat: all figures above come from management commentary on earnings calls. Amazon does not report proprietary silicon as a standalone segment, and no audited data on sell-through rates or capacity utilization has been provided

Why does Trainium matter? Its strategic significance lies not in immediately displacing Nvidia, but in giving AWS optionality over proprietary compute for select training and inference workloads—reducing full dependence on third-party GPU supply, pricing, and lead times. Anthropic is already running core workloads for the next generation of Claude models on Trainium. In theory, rising Trainium penetration could improve AWS unit compute economics—but whether that actually translates into AWS segment margin expansion depends on depreciation cycles, data center utilization, power costs, pricing strategy, and customer discounts. None of these move as a single variable.

This is the biggest hidden variable for understanding AMZN in 2026. The market may not have fully priced in the potential improvement to AWS unit compute costs from rising Trainium penetration—but this thesis still needs validation from subsequent AWS operating margin or capex efficiency data. If AWS gross margins show back-to-back sequential improvement in the second half of 2026, this story gets repriced.

IV. Advertising: A High-Margin Machine Hidden in Retail's Shadow

Amazon's advertising segment posted a figure that's easy to overlook in this earnings release: $17.2B for the quarter. Depending on rounding conventions, different outlets vary slightly, but the commonly cited YoY growth range is approximately +22% to +24%[Investing.com][Yahoo]. Amazon's Q1 release directly disclosed that TTM advertising revenue has surpassed $70B — a scale that makes Amazon Advertising one of the most significant digital ad businesses in the world, yet it still gets overshadowed by AWS and retail in the market narrative.

More important is the margin structure. Amazon does not break out advertising operating margin separately. The market generally assumes advertising's incremental margins are materially higher than those of retail and fulfillment (some sell-side and third-party models put it in the 60%–70% range), but these are external estimates and should not be treated as company-disclosed figures. The directional logic still holds: the marginal cost of each additional dollar of ad revenue is near zero (sponsored search, product placements, Prime Video ads). As this segment's revenue mix has steadily risen from ~7% in 2022 to nearly 10% in 2026, Amazon's consolidated operating margin has been structurally lifted.

Drivers of advertising growth:

- Prime Video Ads: the ad-supported tier launched formally in 2024 and has become a meaningful monetization lever by 2026

- Retail Search Ad Pricing: third-party sellers (~60% of merchandise GMV) are increasingly dependent on sponsored placement traffic

- DSP (demand-side platform) off-site advertising: expanding beyond pure on-site inventory into connected TV and in-app advertising

Priced-In Lens: The market has grown accustomed to 20%+ YoY growth in advertising, so an "ad beat" alone won't move the stock. What could move it is a standalone quantification of advertising's contribution to consolidated operating margin — something most mainstream sell-side models rarely carve out as a separate line item. If analysts begin more systematically modeling Amazon Advertising's OPM contribution, the segment could graduate from "overlooked profit pool" to a fresh valuation catalyst.

V. Tariffs: Jassy's Shifting Tone and the Real Pressure on the Retail Business

At Davos in January, Amazon CEO Andy Jassy publicly acknowledged that tariffs are "seeping into" prices[CNBC]. It was the first time he stated this clearly since tariffs first became a topic in early 2024. Looking back six months later, his language has shifted noticeably — from "we're watching this" to "this is happening."

The specific pressure points:

Seller Side

Third-party sellers account for roughly 60% of Amazon's GMV, a large portion of whom source from China. When tariffs of 10%–25% hit actual FOB prices, third-party sellers have little room to absorb the cost. Some sellers reliant on Chinese supply chains may raise prices by high single to low double digits (based on individual case reports, not platform-wide data).

Fulfillment Fee Hikes (Two Tranches)

Early in 2026, Amazon first raised base fulfillment fees for FBA, Buy with Prime, and Multi-Channel Fulfillment (FBA average +$0.08 per unit) and introduced the DD+7 policy. Then, effective April 17, Amazon added a 3.5% fuel & logistics surcharge on U.S. and Canada FBA shipments, extended to Buy with Prime and MCF starting May 2. In effect, Amazon is passing a portion of its cost increases down to third-party sellers.

Consumer Response

On the Q1 earnings call, Amazon acknowledged observing some consumers trading down (switching to lower-priced SKUs) and deferring big-ticket purchases. This hasn't materially hurt Prime members' purchase frequency in the near term, but it does pressure average order value in the retail business.

Jassy's own words were blunt: "Retail is a mid-single-digit operating margin business to begin with — if costs go up 10%, there isn't much room to absorb that."

The retail segment (1P direct sales + third-party fulfillment + Prime subscriptions) only managed to lift its operating margin to the 6%–7% range across 2025, and that was hard-won.

Scenario Analysis:

- Base case: Tariffs pass through gradually in Q2–Q3, partially offset by seller price increases and fulfillment fee pass-throughs; retail operating margin sees modest compression (on the order of 50–100 bps)

- Bear case: Tariffs, fuel surcharges, seller price hikes, and consumer trade-down all hit simultaneously; retail-related operating margin faces a 100–200 bps giveback risk

This is not the base case — it's a stress test that needs to be validated in Q2 and Q3 earnings.

From a price-in standpoint, the tariff "story" is well known to the market (the Trump administration's tariff policies dating back to 2025, Jassy's repeated comments), but the pace of pass-through has not been priced in. If Q2 results show a meaningful giveback in retail operating margin, the market will reset its models.

VI. Alexa+: The AI Shopping Gateway Sitting on Top of an Estimated 200M U.S. Prime Users

On February 4, Amazon opened Alexa+—its generative AI upgrade—to U.S. Prime members at no charge, ending a waitlist that had run for nearly a year. Non-Prime users can subscribe for $19.99/month[GeekWire].

The strategic significance of this move is widely underappreciated.

Key numbers:

- U.S. Amazon Prime membership base: ~201M per third-party CIRP estimates as of March 2026—not an Amazon-disclosed figure, but sufficient to illustrate the reach Alexa+ could achieve once embedded in the Prime experience

- Users already on Alexa+: tens of millions (per management commentary)

- Opt-out rate during beta: low single digits

- Countries live: U.S., U.K., Canada, Mexico, Italy, Spain, Germany

On May 13, Amazon announced Alexa for Shopping—a unified merging of its existing Rufus shopping assistant with Alexa+'s commerce capabilities, rolled out across the Amazon app, website, and Echo Show devices. Amazon also disclosed that Rufus helped more than 300 million customers research, compare, and purchase products in 2025[Axios].

Rufus was originally an AI assistant embedded in Amazon's product search. By folding it into Alexa+, Alexa for Shopping lets users complete the full purchase journey—product comparison, recommendations, add-to-cart, checkout—through natural-language conversation, bypassing the traditional "open app → search → browse" funnel.

The more realistic monetization path is probably not the $19.99/month subscription (non-Prime users are unlikely to pay for it standalone), but rather using Alexa+ / Alexa for Shopping to lift product discovery efficiency, ad conversion rates, purchase frequency, and Prime ecosystem stickiness.

Why this matters: when AI eventually takes over consumer purchase decisions, whoever becomes the consumer's default AI entry point captures the gateway premium of the next era—just as Google monetized search and Apple monetized the App Store by owning those funnels. Alexa for Shopping is Amazon's bid for that position.

A note of caution, though: in the last voice-assistant cycle, Alexa never meaningfully converted its installed base into a high-frequency commercial gateway, and early market expectations for Alexa+ were neutral-to-skeptical. The current early-penetration signals (tens of millions of users, low opt-out) are encouraging, but translating that into quantifiable revenue contribution likely requires at least two to three more quarters of execution.

Three data series to watch:

- Whether Alexa for Shopping lifts conversion rate and basket size

- Whether AI-driven recommendations push ad inventory pricing higher (CPM / auction clearing prices)

- Whether Alexa+ improves Prime member retention and purchase frequency (churn and visit frequency)

Alexa+ only graduates from "product narrative" to "valuation driver" if any one of these three metrics gets quantified—by Amazon itself or by sell-side models.

Price-in perspective: Most mainstream sell-side models do not currently model Alexa+ as a standalone revenue line, meaning its valuation contribution is likely still being discounted. That creates an asymmetric setup: any upside execution is a positive surprise, while the downside is limited since the Street hasn't built it in to begin with.

VII. Valuation & Price-In: What the $306 Consensus Has and Hasn't Priced In

Here's what the market is actually pricing Amazon at.

Sell-side consensus as of mid-May (41 analysts covering)[Stock Analysis][24/7 Wall St]:

- Consensus rating: Strong Buy

- Average price target: $306

- Median price target: $315

- High target: $370 (Stifel: $319, updated May 1)

- Low target: $175

- At the then-current price, the average target implies ~+13% upside

Don't let the "Strong Buy" label obscure that 13% read — for a trillion-dollar, highly liquid large-cap, 13% sell-side upside is firmly "mildly bullish," nowhere near hot-consensus territory. Compare that to the 40%–60% upside targets Nvidia and Tesla carried at their prior peaks: Amazon simply isn't in that high-conviction narrative channel right now.

What's Already Priced In

AWS sustaining strong growth on AI demand — consensus accepted. Ad revenue continuing to grow ~20% — not news. Anthropic contributing to the AI narrative and some mark-to-market financial gains — already in the mainstream model. Alexa+ not generating meaningful near-term revenue — the market isn't giving it much credit either. The tariff "story" is known, but the pace of pass-through has not been fully priced in.

What Hasn't Been Fully Priced In

Three things that haven't been fully priced in:

First, if Trainium adoption genuinely improves AWS unit compute costs — AWS operating margin could see a structural re-rate upward. This is the single biggest hidden variable in this entire piece.

Second, if the market begins valuing the ad business as a standalone segment — Amazon's overall OPM story gets considerably more compelling. The $70B+ TTM ad business hasn't been carved out as an independent sum-of-the-parts component.

Third, if Alexa for Shopping turns AI-assisted product discovery into a new commerce entry point — Amazon could recapture control over the next-generation consumer traffic layer. Any sell-side analyst who models this independently would need to rebuild the long-term valuation floor for AMZN.

Downside Risks

Not everything unpriced is upside. Three negative variables are equally live:

- The market may be underestimating how long capex will weigh on FCF — if AWS margin recovery isn't visible by 2027, the multiple needs to come in

- The market may be overestimating how reliant Anthropic actually is on Trainium — if the bulk of Anthropic's training/inference workloads stay on Nvidia, the "closed-loop" thesis softens

- The market may be underestimating tariff and 3P seller margin pressure on retail margins — Q2/Q3 earnings will be the ground truth

Taken together, AMZN's current valuation reflects a **"complete narrative, measured pace, room for upside surprise but near-term capex overhang"** setup. This isn't a screaming buy, but it's not a name to avoid either.

八、接下来 3 个季度,市场真正会看什么?

Before the risk checklist, here are the actionable metrics OurAlpha will be tracking closely across Q2–Q4 earnings:

First, whether AWS growth can hold in the 25%–30% range. If Q2/Q3 slips meaningfully below 25%, the market will question whether Q1's 28% was a one-off acceleration rather than a new baseline driven by AI workloads moving into production.

Second, whether AWS operating margin can stay stable — or improve sequentially — despite elevated capex. The entire investment thesis around Trainium ultimately comes down to unit compute costs and segment-level margins.

Third, whether free cash flow shows signs of bottoming in H2 2026. If FCF stays depressed for an extended period, Amazon risks being re-rated from "high-quality growth stock" to "capital-intensive infrastructure play."

Fourth, whether the advertising business sustains 20%+ growth and earns a standalone valuation line in sell-side models. Advertising remains Amazon's most consistently underappreciated profit pool.

Fifth, whether Alexa for Shopping discloses any data on conversion rate, basket size, ad auction dynamics, or Prime retention. The moment any one of those metrics gets quantified, Alexa+ could shift from "product narrative" to "valuation input."

Across these five indicators, any marginal change in any one of them will force sell-side model re-ratings. Both the entry and exit cases ultimately hinge on exactly these data points.

IX. Risk Checklist

Near-term (3–6 months):

- Free cash flow continues to be suppressed by capex, with valuation compression expected as the narrative shifts from "growth stock" to "infrastructure stock"

- The actual Q2 tariff impact on retail operating margins

- AWS quarterly growth falling below 25% (any sequential deceleration would be a negative surprise)

Medium-term (6–12 months):

- Whether the Trainium adoption curve ramps as expected, which will determine the pace of AWS gross margin improvement

- Anthropic valuation swings flowing through EPS via mark-to-market, creating significant quarter-to-quarter earnings volatility

- Policy environment shifts post-U.S. election (regulation, taxes, tariffs)

Long-term (12+ months):

- How quickly AI compute ROI bottoms out industry-wide (a sector-level risk, not unique to AMZN)

- Whether Alexa+ can genuinely become the "AI-era shopping gateway," or prove to be yet another failed attempt

- Third-party seller attrition (tariff pressure driving migration to Shopify / TikTok Shop / Temu)

X. What Are You Actually Buying When You Buy Amazon?

Pulling all the threads together, Amazon in 2026 is essentially three things in one:

First: A strong current cash flow machine spanning retail, advertising, and subscriptions ($700B+ annualized revenue, operating margins expanding), which anchors the valuation floor.

Second: A capital-intensive AI infrastructure giant in the midst of heavy reinvestment, where the story over the next 3–5 years is capacity ROIC (AWS + Trainium + data centers), providing long-term upside.

Third: A potential AI consumer gateway not yet fully priced in (Alexa+ / Alexa for Shopping / Rufus + 200M+ Prime members), representing asymmetric optionality.

Near-term, the valuation overhang is capex intensity and the FCF trough timeline. The medium-term re-rating catalyst is Trainium penetration and advertising OPM expansion. The long-term ceiling depends on whether Alexa for Shopping can genuinely lock in the next generation of consumer commerce.

Amazon today is neither cheap enough to buy with your eyes closed, nor something to avoid out of capex anxiety.

It's better described as a super-platform using retail, advertising, and subscription cash flows to finance the next generation of AI infrastructure. Near-term, the market watches FCF and capex; longer-term, it will reprice AWS, Trainium, and the AI shopping gateway.

For AMZN in 2026, the real question isn't "is there an AI story" — it's whether this $200B capex cycle can be proven to generate sufficiently high returns.

The thesis is intact, the valuation is neutral, and the outcome hinges on ROIC.

A Note on Data Sourcing

Amazon does not separately disclose the following: AWS AI services revenue, Trainium / proprietary silicon revenue, advertising segment operating margin, or Alexa+ direct revenue and monetization metrics. Accordingly, all estimates in this article regarding AI run-rate, custom chip ARR, advertising margins, Trainium penetration, and Alexa+ commercialization are analytical inferences based on public disclosures, management commentary on earnings calls, and press coverage — not official Amazon segment financials. Readers using these figures for investment decisions are encouraged to cross-reference against Amazon's 10-Q and 10-K filings directly.

Sources

- Amazon Q1 2026 Earnings Beat as AWS Growth Hits 15-Quarter High — Yahoo Finance

- Amazon Q1 2026 Slides: AWS Surges 28%, Record Margins Offset by Capex — Investing.com

- Amazon to Invest Up to Another $25 Billion in Anthropic as Part of AI Infrastructure Deal — CNBC

- Amazon and Anthropic Deepen AI Ties with a $100B AWS Commitment — The New Stack

- Amazon $200B 2026 Capex: Inside the AWS AI Buildout — AlgeriaTech

- Amazon Q1 Revenue Hits $181.5B but $16.8B Anthropic Gain Inflates Net Income — The Next Web

- Amazon CEO Jassy Says Trump's Tariffs Have Started to 'Creep' into Prices — CNBC

- Amazon Rolls Out Alexa+ to All U.S. Customers, Making AI Assistant Free for Prime Members — GeekWire

- Amazon Pushes Alexa Deeper Into AI Shopping with Rufus Integration — Axios

- Analysts See $20 of Upside for Amazon Stock Even at All-Time Highs — 24/7 Wall St

- Amazon.com (AMZN) Stock Forecast & Analyst Price Targets — Stock Analysis

This article is for informational and research purposes only and does not constitute investment advice. All data as of 2026-05-13. Market views and ratings reflect OurAlpha's current judgment and are subject to change as future earnings results and market conditions evolve.

This content is for informational purposes only and does not constitute investment advice, trading advice, or any guarantee of returns.